Trustage Life Insurance Review 2024 Worth it?

Posted in Burial Insurance Carrier Reviews last updated on January 2, 2024

Posted in Burial Insurance Carrier Reviews last updated on January 2, 2024Is trustage life insurance a real insurance company? No, they are actually an agency they also only work with one life insurance company instead of working with multiple life insurance companies to guarantee the lowest rates possible. This is the problem with a lot of these captive agencies that assist millions of people.

We have seen similar issue’s like this with Colonial Penn, Globe, AARP, Lincoln Heritage and much more.

Now that being said are there positives to Trustage life insurance? Yes but it is important to be well informed about this agency and their product so you can make an informed decision.

This is the bottom line when it comes to protecting your loved ones with insurance. Getting the right policy that fits your needs is the key to protecting the financial future of your loved ones.

In this article, we will go over everything you need to know about trustage life insurance.

Table of contents

Is Trustage insurance any good?

Is trustage life insurance legit? Yes, their coverage is legitimate life insurance however compared to other companies it is not as competitively priced as we will demonstrate later. That being said trustage understands the importance of life insurance just like anyone else.

All Insurance policies are designed to help people by helping protect their income when a family member in the household dies.

Based on the ability of the insurer and their claims-paying ability life insurance would provide a death benefit payout to a family for either paying a mortgage, funeral, or any outstanding debts.

You can usually learn about the claims process by asking the life insurance company directly. This is also reflected based on the claims record of the carrier this is represented in their reputation.

Basically, if a carrier has paid a lot of claims they are a solid company.

So here are some things to consider about Trustage life insurance

- Typically overpriced compared to other products

- Strict Underwriting can make it hard to qualify for their product

- They only have one life insurance company to offer their customers

There is also no agent to help you with your purchase, the entire application process is done online and does not require a medical exam.

Now, this may be convenient but without working with an expert-level agent this can also be very bad because you are not guaranteed to get the best product.

The Pros & Cons

There are really only 2 pros to Trustage life insurance and they are as follows:

Pros

- Quick online application to apply for coverage

- Guaranteed Acceptance Whole Life Insurance with Trustage No Health Questions

- No Medical Exam Required

Cons

- Guaranteed Acceptance Whole Life Insurance from Trustage has a 2 year waiting period

- Guaranteed Issue Whole Life Insurance from Trustage is more expensive than other life insurance companies

Trustage Life Insurance Products

How does Trustage life insurance work? All life insurance works the same, you get a policy and if you die within either the term period for a term policy or when you die if you have a whole life policy they will both pay a death benefit to your beneficiary when a certificate of death received.

Trustage has 3 different Types of Plans

- Guaranteed Issue Whole Life Insurance

- Simplified Issue Whole Life Insurance

- Increasing Premium Term Life Insurance

Now their whole life products are very straightforward

The whole life plans have:

- Fixed Premiums – Price never increases

- Level Death Benefit – Death Benefit never decreases

Their Term policy is the real gimmick out of the bunch in our opinion because it has premiums that increase every 5 years. This means within 10 years your term coverage can become unaffordable and you will have to drop it because of the expense.

This is why if you need a term policy with a fixed premium that never increases call us we can assist with the best term options available.

Now both the simplified issue and guaranteed issue whole life policies from Trustage are considered Trustage final expense insurance. These types of policies with smaller benefit amounts and simplified or no underwriting are designed to cover funeral and other end of life expenses.

That is why you will see products like Trustage’s final expense insurance being referred to as burial insurance, funeral insurance and cremation insurance. They mean the same thing which is life insurance for funeral expenses.

Trustage Whole Life Insurance

Trustage Guaranteed Acceptance Whole Life Review

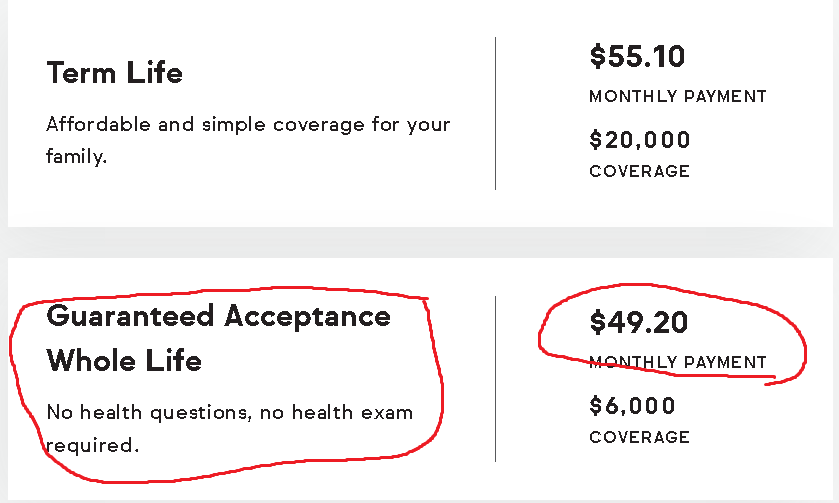

We went to their website and ran a quote on ourselves and the first 2 options offered to us were their term life or guaranteed acceptance options. You have to actually click on the guaranteed acceptance option to see more coverage and get to the simplified issue policy that has no waiting period.

This both confused and frustrated us.

Their guaranteed acceptance policy does not require a medical exam and has no health questions. Now this may sound good but all guaranteed issue policies with no health questions have an automatic 2-year waiting period.

This means if you die within the first 2 years the only thing your family gets are the premiums paid into the plan plus 10%.

What if you die tomorrow? This type of plan will not do your family any good. Now there may be factors with your health that will make guaranteed acceptance your only option however we also compared Trustages GI with American General and AIG is much more affordable so is Gerber life.

Some features of Trustages Guaranteed Issue policy are:

- Builds Cash Value

- Covers Ages 45 – 80

- Coverage Range from $2,000 – $20,000

- It is not available in New York or Washington

Again American General and Great Western are superior to this product in many ways.

Trustage Simplified Issue Whole Life Review

Now this is a decent plan however it still cannot beat the prices of Mutual of Omaha. That being said there is no waiting period for this policy they look at your medical history and analyze your medications. If everything checks out you are approved.

In addition to this Trustages underwriting is quite strict according to clients and other Trustage life insurance reviews. This is very common with companies that have only one product and take a “one size fits all approach”.

Some features of this plan include:

- Cash Value is Built

- Covers Ages 18 – 85

- Coverage Ranges by Age

- Age 18 – 70 $5,000 – $100,000

- Age 71 – 75 $5,000 – $50,000

- Age 76 – 85 $5,000 – $25,000

- Montana & New York States the product is not available

Again Mutual of Omaha has this product beat because even at age 85 MOO can offer $30,000 or more in coverage.

Now on a positive note Trustage does offer $100,000 in coverage to seniors age 70 or younger. Keep in mind that Mutual of Omaha Living Promise is always going to be cheaper than Trustage.

You can learn more about options over 80 here.

Trustage Term Life Insurance Review

What is Trustage Term Life Insurance? This plan is a lot like the kid on the playground that has lice that none of the other kids want to play with. We don’t see really any benefit to this other than the quick approval process that is done online.

That being said if you work with one of our agents they can help you get a term policy with instant approval and no medical exam.

The features and massive cons in our opinion are:

- Policy expires at age 80

- Premium increases every 5 years

- Available to ages 18 – 69

- Coverage ranges of $5,000 – $300,000

- State of New York not Available

If you do get approved for Trustages term life policy after they medically underwrite and qualify you there are no waiting periods for this coverage.

We do not believe any consumer should go for an increasing term product considering all of the better term options out there that have premiums that never increase for the length of the term.

Now all of these products from Trustage are underwritten by CMFG Life Insurance Company and CMFG is a good life insurance company with a lot of agents working with them but if Trustage offers only one company this is how they miss the mark.

Trustage Financial Ratings

The financial ratings for Trustage are solid for the most part which is a good thing. Trustage financial ratings are as follows:

- A.M. Best Rating – A (Excellent)

- Truspilot Rating – 4.7 out of 5 stars with 6,884 customer reviews as of 5/21/2023

Trustage Reviews BBB

The BBB rating for Trustage is 1.82 out of 5 stars with 48 customer complaints closed in the last 3 years. In addition to this they have had 33 complaints closed within the last 12 months as of 5/21/2023. They have a lot of negative customer reviews from recently in 2023.

How to Cancel A Trustage Life Insurance Policy

According to their FAQ’s section for customers, you must call Trustage directly to cancel your Trustage life insurance policy. They do not offer a way to cancel a policy through their website portal.

Is Trustage Worth it?

No in our opinion it is not from a consumer stand point. If you want the most affordable best priced policy you need to work with an agency that represents multiple life insurance companies.

In addition to this having highly trained agents that understand the underwriting niches for the carrier to get you coverage with no waiting period.

How Good is Trustage Insurance?

In our conclusion not very good, the quick online application process and approval is good but the pricing should be more competitive and with the limited option of one company you are better off looking somewhere else.

Trustage Background & Contact Information

Trustage is a brand of CMFG Life Insurance Company and both are owned by CUNA Mutual Group. All of Trustage’s life insurance products are underwritten by CMFG Life Insurance Company. Many life insurance companies utilize this same practice.

Trustage exclusively partners with credit unions which makes it unique it also does not partner with any traditional banks. They have over 3,500 credit unions they are partnered with in the USA. You do not have to be a member of these credit unions to purchase Trustage coverage.

Trustage also offers auto & home insurance because they are partnered with Liberty Mutual insurance. Those would be their other life insurance offerings. Credit Union members can get Trustage accidental death plans for free by being members.

Trustage Contact Info

- Website: https://www.trustage.com/

- Consumer Information Number: 800-428-3932

- Other Phone Number: 1-877-649-1311

- HQ Address: 5910 Mineral Point Road, Madison WI 53705